UK Industry Prepares For Policy Changes As Capacity Doubles

During the first half of 2014 (1H'14), the U.K. solar photovoltaic (PV) industry deployed 1.47 gigawatts (GW) of new capacity, which exceeds the amount of new capacity added during 2013, which was a record year for the U.K. solar PV industry. This was according to a recent update from NPD Solarbuzz.

The U.K. is now firmly established as the leading solar PV market in Europe, and the country is expected to become the fourth largest global market for new solar PV deployment in 2014.

New capacity added during the first half (1H) of 2014 was dominated by first quarter (Q1) activity that accounted for approximately 80 percent of the total; this quarterly split was caused by the drop in Renewable Obligation (RO) incentives for ground-mounted PV from 1.6 to 1.4 on April 1, 2014

The residential segment continues to trend at 80 megawatts (MW) to 100 MWs per quarter, with the industry having adapted successfully to the degression mechanism implemented earlier by the Department of Energy and Climate Change (DECC)

The commercial rooftop market remains heavily underutilized, despite DECC's aspirations to shift solar PV installations from the ground onto rooftops; large rooftops (above 100 killowatts) accounted for just 4 percent of capacity in 1H 2014

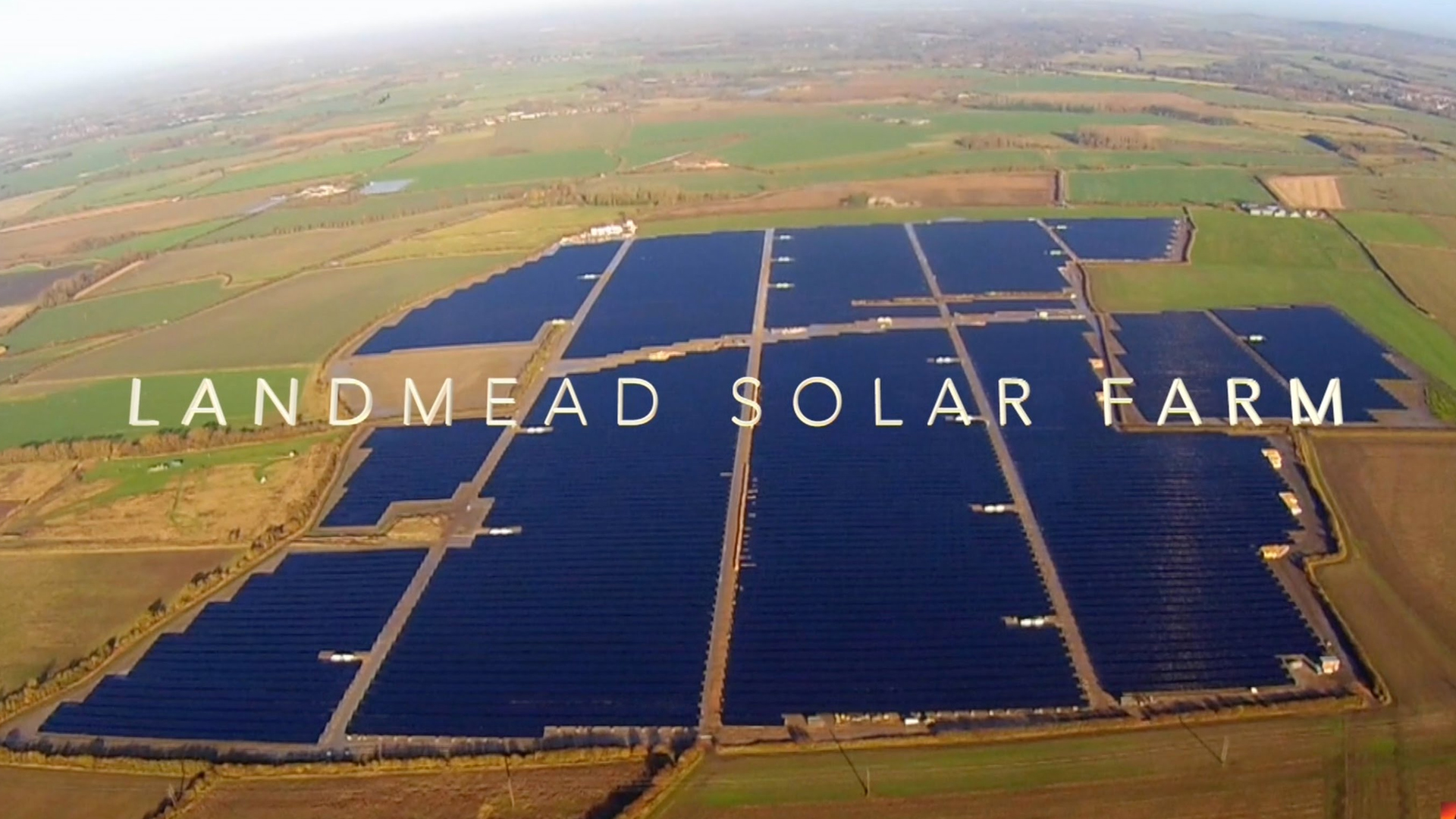

The ground-mount segment was the big winner during 1H 2014, accounting for more than 75 percent of new solar PV capacity deployed; solar PV farms remain the most attractive option for investors seeking to accumulate large portfolios of PV assets

The U.K. PV industry is currently adapting to recent proposals from DECC to cut RO funding two years earlier than expected, for ground-mounted projects above 5 MW in size. This change is driving a rush to complete as many ground-mounted projects as possible before March 31, 2015. It is also creating serious concerns for some legacy project developers who face the prospect of reduced revenues next year, and possibly even bankruptcy.